The good news is that those debt costs will drop by more than 42%, to less than $8 million, starting in the 2018-2019 school year. Woo hoo!

The problem is that the school district is under a great deal of financial stress right now. Last year’s budget included cuts to all school buildings, the use of reserve funds, yet still required a tax increase. The coming budget looks like more of the same: Employee retirement benefit costs are estimated to rise again by almost 15% — an amount set by the state but borne by local taxpayers. The district is also required by law to hire two additional special education teachers because of rising enrollment in special education programs. This is all on top of the fact that the politicians in Harrisburg continue to hold up funding to local school districts, which makes up almost 20% of East Penn’s revenue.

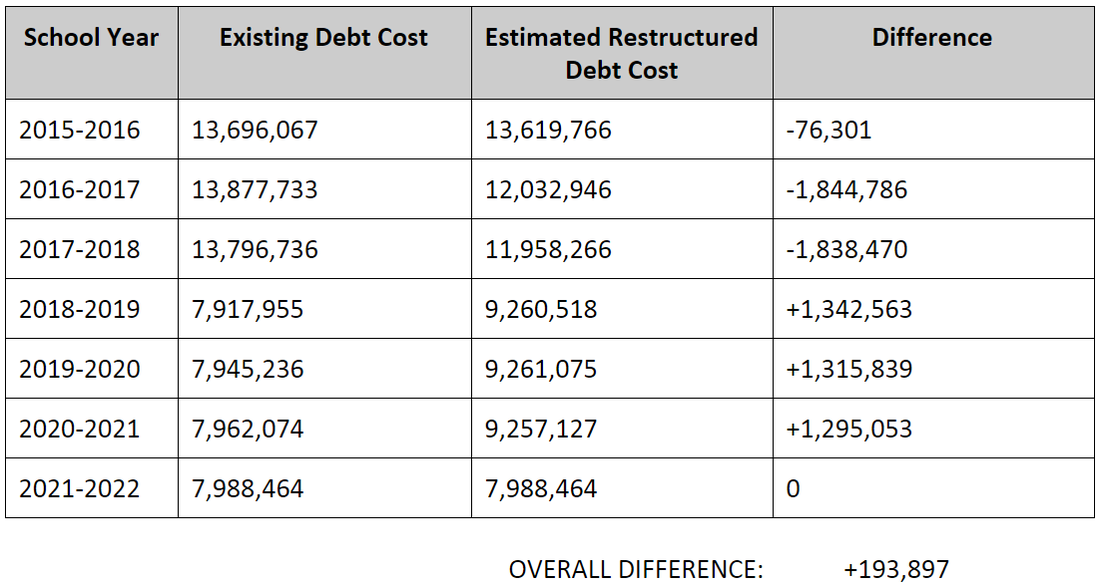

In order to at least partially address these issues, the district administration has put forward a proposal to restructure some of the district’s debt. The restructuring would provide immediate debt relief over the next couple of years, freeing up millions of dollars that could be used to cover these other costs. But alas, there is no such thing as free money. The restructuring would actually cost taxpayers more money in the long run — to the tune of about $200,000. The current restructuring plan produces short terms savings but at greater overall cost in the long term.

There are some very good reasons to adopt this restructuring plan:

- The plan would reduce the immediate pressure on taxpayers.

- It would help fix the structural deficit and restore last year’s funding cuts.

- It would help pay for a number of immediate district needs.

On the other hand, there are also some very good reasons to reject the restructuring plan:

- Most importantly, it will cost almost $200,000 more over the long run.

- It reduces the debt relief the district could enjoy beginning in 2019.

Let me say a little about this last point, because it’s important: In two years, the district will pay $5.8 million less in debt payments. That “extra” $5.8 million could be used for initiatives of importance to our community. A tax cut, for example. Or a program to ensure every child has access to a computer at home. Or all-day kindergarten. If we restructure the debt now, the district will only realize a debt savings of $2.7 million in 2019. That money, while significant, won’t stretch as far for community priorities.

PS: There is an important distinction between this restructuring proposal and the debt refinancing the district has done several times over the last two years. The refinancing has lowered the interest rate the district has to pay on its debt, saving taxpayers hundreds of thousands of dollars each time. These are real savings. By contrast, the restructuring plan gives us short term relief but at a greater overall expense.

Actually, by chance, I just sent an email to the full EPSD board asking members if there wasn’t a bond issue available to be refunded or restructured at this moment, would they think it wise to borrow $1.8 million+- in each of the next two years to finance current costs and pay it back in years three through five? That’s really what’s happening here.

That $193,897 extra interest to be charged due to the restructuring is a pittance against the current 7-year repayment plan of $73.184M, representing a hike of only .26%. You don’t go into financial detail to explain the current stress on our budget, but if significant enough, I certainly think the restructuring is very fair given the payment reduction over the next couple of years. So to me, it all depends on how tight things are right now.

A very good question!

Partially agree about interest cost, but I would compare that $193k to the $3.8 million cash flow benefit that derives from the restructuring of this one bond issue, and not with the $73 million of payments required for the dozen or so bond issues which that covers. (the remaining bonds are unaffected and we should look only at the increments to be meaningful) In my note to school board I said: “1) Interest rates are so low that any additional interest cost from delaying principal payments in the restructure option is relatively trivial; however, similarly, there’s no real likelihood of paying back with cheaper dollars with continued low inflation or theoretical PV discount rates.”

More important is the fact that they are proposing essentially to borrow more to skip payments. My note says “2) In the absence of a regular bond refinancing, would EPSD really be considering borrowing $3.6 million over the next two years to pay current bills, and paying the money back in years three through five? If one looks at it that way, the restructure almost wreaks of desperation.”

You’d have to ask the board why they seem to be so desperate to do this. If anyone did this in their personal finance (and we know many who did this leading up to the financial crisis), it would be a red flag.